Fiscalization and Real-Time Reporting in the Netherlands

The Netherlands has no certified POS requirement, but VAT businesses must keep accurate transaction records for tax audits.

The Netherlands does not have a formal fiscalisation system for cash registers or POS software. VAT-registered businesses that record customer payments are not required to use certified or government-approved POS systems, but must keep accurate, complete, and reliable sales and VAT records.

Under Dutch tax law, VAT-registered businesses must keep their sales and financial records organized and accessible. Records like invoices, receipts, and transactions should be stored safely for the required period so they can be checked during audits. Digital records are allowed, but they must stay readable and unaltered throughout the retention period.

In the Netherlands, there isn’t a fiscalisation system like in France, so businesses don’t have any certification deadlines for cash registers or POS software. However, Dutch tax law still requires VAT-registered businesses to keep their sales and financial records organized and safe. These records must generally be kept for at least 7 years, and in some cases up to 10 years, so they can be checked if needed. This applies whether the records are on paper or stored digitally.

Tired of scrolling through information about e-invoicing?

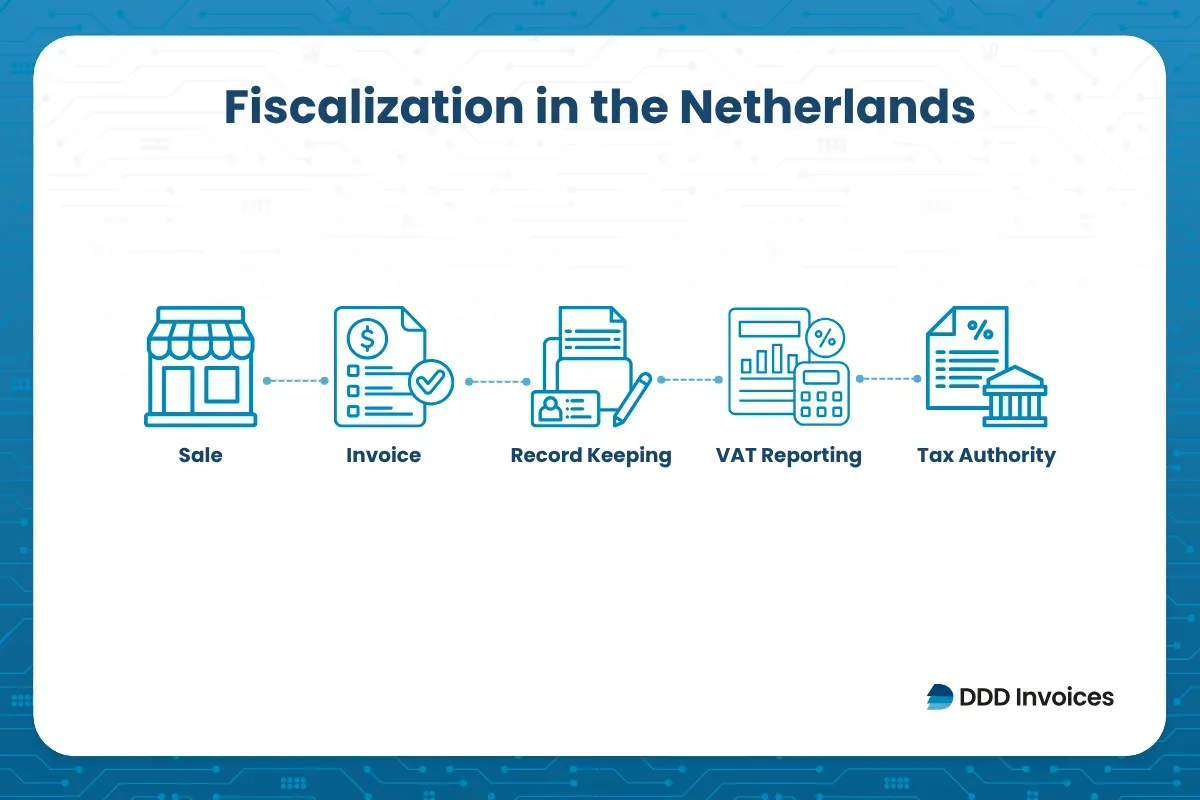

Fiscalisation is the system of rules and practices in the Netherlands that ensures business transactions, sales, and VAT-related data are properly recorded and traceable for tax purposes. It’s about ensuring that VAT and other tax-relevant information from every transaction can be verified by the tax authority if needed. Fiscalization focuses on keeping sales data accurate and trustworthy, so taxes are reported correctly and businesses comply with Dutch tax law.

All businesses selling goods or services must provide invoices with the date, unique number, VAT amount, and other required details. Invoices help make VAT reporting clear and correct, and they must be issued by the 15th of the month after the sale.

E-invoicing in Netherlands means sending invoices in a digital, structured format instead of paper. It is mandatory only when supplying the Dutch government, while B2B and B2C e-invoices is voluntary as long as they follow VAT rules.

Starting 1 January 2026, Dutch shops that offer VAT refund services to travelers from outside the EU must use a digital process to register the VAT refund information. This digital system replaces older paper‑based methods and makes it easier for customers to claim VAT refunds using a digital app.

There is no fiscalisation system in the Netherlands, so businesses aren’t fined for cash register or POS certification. But they must follow VAT rules. Filing a VAT return late or not at all can lead to a penalty of around €82, and incorrect or incomplete returns can result in higher fines, sometimes several thousand euros. Serious cases of VAT fraud may lead to even larger penalties or legal action.

Handling fiscal obligations in the Netherlands means keeping up with VAT invoicing rules, e-invoicing for government contracts, and proper record management. DDD Invoices helps businesses meet Dutch tax requirements and stay prepared for audits or digital reporting obligations.

We make it easier to keep accurate, audit-ready records and adapt to evolving VAT rules without disrupting daily operations. With DDD Invoices, businesses can focus on growth while staying fully compliant with Dutch tax law.

No. The Netherlands does not have a formal fiscalisation system that requires certified cash registers or POS software. Instead, businesses must follow general VAT and invoicing rules set out under Dutch tax law.

E‑invoicing in the Netherlands is mandatory when supplying the Dutch central government or other public authorities. For regular business‑to‑business or business‑to‑consumer transactions, e‑invoicing is currently not compulsory, and businesses may use paper or digital invoices that meet legal VAT requirements.

All businesses that sell goods or services and are liable for VAT must issue invoices that include required details such as invoice date, a unique number, price, VAT amount, and VAT identification number regardless of whether they are paper or digital.

If a VAT return is filed late or incorrectly, the Dutch tax authorities can impose penalties. For example, a late VAT return can result in a penalty (often around €82), and repeated or serious errors can lead to higher fines or further action.

In the Netherlands, ticketing systems for events must follow standard VAT invoicing and reporting rules. Ticket sales are treated like other sales for VAT purposes, and businesses should ensure they issue valid invoices and report VAT correctly on those sales.

Yes. Foreign companies that are registered for VAT in the Netherlands must follow the same VAT invoicing, reporting, and record‑keeping requirements as Dutch businesses.

Written by the Compliance & Growth Team

Reviewed by Denis V. P.

DDD Invoices is an enterprise-grade platform delivering a powerful infrastructure for creating, sending, receiving and storing electronic documents. DDD Invoices enables software providers like ERPs, SaaS, eCommerce, POS systems, accounting & invoicing softwares, billing services and others, to easily adhere to global invoicing compliance requirements and shorten their time-to-market.